Everyone Needs a Steady Infusion of New Content

“Fight for honor! Fight for the man beside you! Fight for those who bore you! Fight for your children! Fight for your future! Fight for your name to survive! Fight! For immortality!” Theseus, “Immortals,” Relativity Media, 2011

Growth Everywhere – Appointment TV may not dominate today’s at home entertainment but it’s still the first choice for folks to watch in certain parts of the globe and of a certain age. (Yes, they probably have more disposable income than your Gen Zers.)

Not bad for the movie/series delivery marketplace if it were all one market and if the only people competing for the streaming market were the big five – Netflix, Disney (Disney+), WBD’s (Warner Bros Discovery) HBO Max, Amazon (Prime), Paramount +.

That ain’t the case!

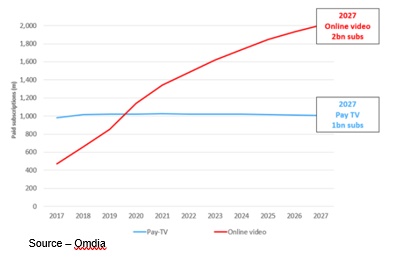

Not long-ago research firm Omdia projected that global SVOD subs would increase to nearly 1.5B by the end of the year and pay TV would remain relatively level at 1.03B.

It’s really 195 markets with hundreds of different home/personal entertainment providers, each vying for their own portion of “targets” – 7.96B people, 5.4B TV viewers – most available to any/all content delivery folks.

Sure, there are a few exceptions:

- Russia has 145M people, 46.6M TV households but the only organizations reaching them are…Russian

- China has a population of 1.414M people, 427M TV households and a government with a very tight control over who serves them -- Tencent, iQiyi, Youku, Mango, Bilibili and government supported services. The services are working on getting more subscribers in APAC (Asia Pacific) but it’s not a two-way relationship.

Beyond Reach – While it’s great to look at people who want to stream their content as one big marketplace, we tend to forget that geopolitical activities also play an important role in what people watch – or don’t watch – on their screens.

Still, that’s a pretty big pay TV/SVOD market.

Of course, when it comes to appointment TV, the market is flat, shrinking slightly. It’s growing in some areas like India, Africa, APAC, LatAm; shrinking in other areas such as North America, EU.

Pay TV is a mature industry that isn’t attracting new competitors while still producing good profits for established players.

TV On Time – In many emerging countries, Pay TV is very economic and if you can only afford one choice, you tend to pick the one with the most predictable options--even when you might prefer anytime, any screen viewing.

The bundled linear TV arena has just enough long- standing content to keep its parental/millennial plus market happy with them such as CBS – The Amazing Race, FBI series, Big Brother, Survivor, the NCISs, Blue Bloods; BBC – This Country, Young Offenders, In My Skin, Ladhood, Shrill; Fox TV – News, Simpsons, 911s, MasterChef; France’s TF1 – sports (football, rugby, motorsports), The Voice, Mask Singer, Paw Patrol, Toy Castle; Australia’s Channel 7 – News, RFDS, Yummy Mummies, SAS Australia, sports, Flushed, It’s Academic.

Long-standing franchise series have been good for the networks, local stations and advertisers. The folks who like them, really like them.

Disney has a rich library of brands – Pixar, Marvel, Star Wars. WBD has DC, Warner Animation, Wizarding World, Game of Thrones, Potter-verse.

Discovery is also juggling old-school, new-school businesses with long-running down-market programs like Travel Channel, Motor Trend, Animal Planet, Magnolia Network, OWN and other properties to retain established audiences while reaching out to capture new anytime, any screen viewers.

And WBD has to do all of this while servicing its $55B acquisition debt on top of CEO David Zaslav’s very nice $246M annual salary.

They and the other streamers – including Amazon Prime, Netflix, Apple, Telemundo, Hulu, Acorn, Salto, Britbox, DAZN – have taken big hits on their stock value and have said they’re going to cut back on their new project budgets.

Sure, but they need a constant supply of fresh content to attract and keep new subscribers nationally and internationally.

When Netflix “shocked” the financial market earlier this year saying they had dropped 200,000 of their more than 221.8M worldwide subscribers (including 700K Russian subscriptions), they announced they were going to “moderate” their content creation budget and examine subscriber options (AVOD).

One by one, all of the Hollywood/tech streamers agreed that they were also going to pare back on their portion of the industry’s $240B movie/TV show creation budget.

Almost in unison, WDB’s Zaslav, Paramount’s Bob Bakish, Disney’s Chapek, Netflix’s Ted Sarandos and others said they were going to be more focused on how much they were spending on new content to attract new subscribers.

Managing Investments – Nearly every technical, studio and network streaming service has told the financial community they are going to more closely monitor their new content investments, but it is a little difficult when there is pressure for them to grow their subscriptions quarter over quarter with new content.

The pronouncements sent a lot of production studio owners; A/B Listers; content creation, production and post folks to double-check their overhead and personal budgets.

Netflix’s Sarandos said they would continue investing even as the firm’s CFO said they were pulling back--including layoffs, dropped projects and savings in other areas.

WBD’s Zaslav has said numerous times that the company isn’t going to overspend to drive subscriber growth. At the same time, he’s making significant adjustments in his organization and staff to produce budget savings of more than $3B in business overhead areas.

Paramount’s Bakish straddled the line saying they would spend less than the competition to build Paramount + but they would continue to ramp up their investment.

Disney’s Chapek, who has made a few missteps (‘don’t say gay,’ park workers salaries/attire, staff realignments) said his team would monitor content cost growth, squeeze more profits from its streaming platform and increase the firm’s focus on creativity and inclusion.

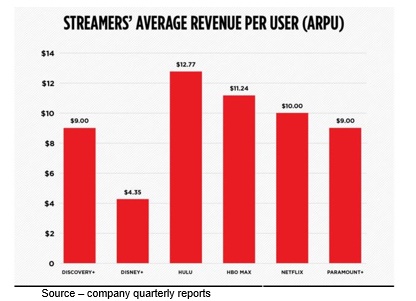

New vs. Existing – The financial community focuses on how many new subscribers a streaming service can capture each quarter because growth is exciting. However, ARPU (average revenue per user) is a more accurate view of how well the various services are doing. Churn is expensive.

All of the streaming bosses switched their focus from bragging about national/international subscriber increases and totals to ARPU (average revenue per streaming user) or the value of their continued content investment.

Everyone agrees there are too many streaming options and the cost for the services is becoming unbearable for consumers who cut their cable bundles ($100+) to go with a more satisfying and more economic streaming solution.

Budget Cap – Every streaming service is positive that their content is more valuable – and more desirable – than the next guy’s/gal’s but people are rapidly finding their home entertainment services are quickly costing them as much as what they left behind when they cut the TV cord. The challenge is to make hard decisions to drop services or, better yet, shift to lower-cost ad-supported services.

Surveys around the globe have consistently emphasized that four or more streaming services are too many and that service brand loyalty comes from building community, creating a must watch viewing experience and an acceptable streaming service price range, including an acceptable trade-off of accepting ad-support for service savings.

Budget Decisions – As anytime, any screen streaming becomes more commonplace, people are evaluating the services they have and consider on the volume of new content that is available that interests them as well as how much ad-free viewing is really worth. People are increasingly coming to realize that watching a few ads isn’t all that bad.

Consumers worldwide – but especially in the Americas – have gained enough experience in watching what they want, when they want, where they want that they have established their own value proposition for the content they view.

With the ready abundance of new services and new content combined with their overall home entertainment budget, they are increasingly developing their own decisions when they follow Kenny Rogers advice, “You've got to know when to hold 'em. Know when to fold 'em. Know when to walk away.”

Increases can only spur consumers to reconsider the number of subscriptions they need and can easily make snap decisions on which service(s) deliver the best ratio of new, interesting content along with the trade-off of cost – subscription and ads.

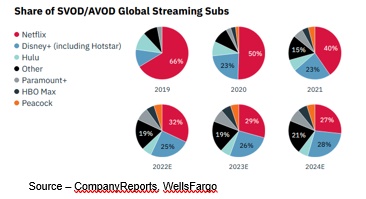

Bigger Pie – With the entry of Disney, WBD’s HBO Max and others into the streaming market, more and more people are moving to the what-I-want, when-I-want it entertainment. Solutions folks often view their subscribers coming at the detriment to Netflix growth but that isn’t necessarily true because the available market is growing. In addition, most consumers have multiple services they subscribe to so everyone benefits.

For our content creation, participation, production/post friends, few industry insiders believe the promised cut back in content spending will happen.

The old-line studio and TV moguls as well as the tech leaders know that theatrical and appointment TV opportunities will remain relatively level with predictable growth maintenance based on the acceptance of tentpoles and franchises.

However, the long-term growth potential for Netflix, Disney+, Paramount+, HBO Max, Hulu, Peacock, Amazon Prime and Apple TV+ is dependent on gaining and maintaining customers.

Even Wall Street analysts/forecasters know you don’t get anywhere by standing still.

Content growth and continued investment are not only necessary, they’re vital.

As Zeus said, “It's not living as such that's important, Theseus. It's living rightly.”

Is life worth living without a good story to tell and a ready audience to view it?