You're right, Ruben. The world does keep moving and it can be a damn cruel place. Joe - Sound of Metal, Amazon Studios, 2019

We are a little over halfway through 2021 and surprise, the content industry not only survived the pandemic but in many ways is thriving because of it.

We realize that a year ago at this time the industry was in the middle of the Canadian sitcom Schitt's Creek without a proverbial paddle, but despite a lot of battle scars and a lot of hard work, it is back and in many ways better.

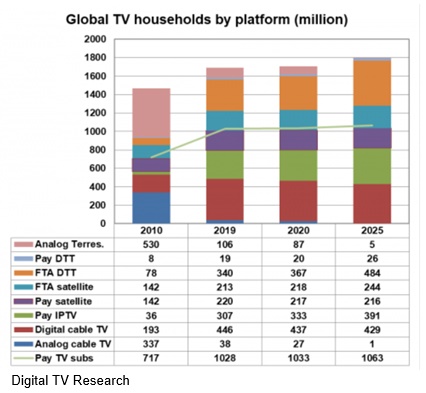

While folks in the Americas like to say pay TV is dead and everyone is cutting the cord, it has leveled off in most countries and actually increased in others.

Â

Day, Hour While pay TV has fallen out of favor in the U.S., it has maintained its global position in the entertainment arena and even inched up ever so slightly.Â

Okay, so pay TV didnt break any records; but they maintained their position and learned hopefully that if you want to be around for the long haul, you have to pay attention to and not abuse your customers.

They learned the latter point the hard way by watching streaming services both in their country but also from outside their borders sweep in, convince folks to cut the cord, get rid of the shows and services theyre not interested in (save $$$$) and enjoy a show movie/series without 20 minutes of ads every hour and enjoy the programming wherever and whenever they wanted on the screen of their choice.

While the shift affected Comcasts TV bundle as folks weighed whether or not the channels were worth saving, it also gave the worlds largest home connection service a boost.

Sixty percent of the people who shifted to or added a streaming service signed up for Comcasts very profitable internet-only service, making way for their wireless telecom and smart home services.Â

Oh yeah, the company also owns Europes Sky broadband and pay TV services.

Â

Growing Flow People around the globe have warmed up to the idea of watching what they want, when they want and on the screen they want. As services approach the maximum number of TV households, consumers add and subtract sources to their personal bundles.Â

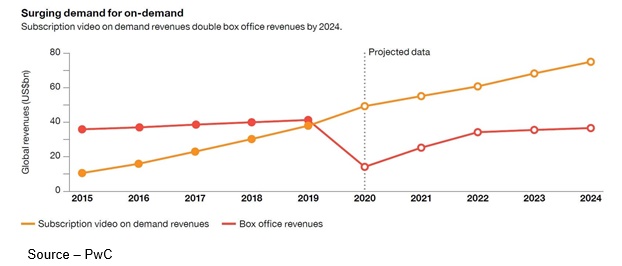

As a result of the viewing shift, SVOD subscriptions have nearly doubled from 650M at the end of 2020 and is expected to grow to 1.25B by the end of 2024.Â

By comparison, global pay TV subscriptions surpassed 1B in 2018--arguably the services peak.

With the present exception of China, individuals and their households around the globe are now viewed as potential streaming subscribers.Â

Chinas anywhere/anytime/ any screen market is tightly controlled by the government with the leading services being:

Tencent 900M subscribers

iQiyi 500M

Youku â 500M

Â

Minimizing Churn Being early and being aggressive in the streaming arena has been important for a few of the services but the key will be how well they capture and retain subscribers. Other services will have more modest subscription bases and do well with specialized focus.Â

While the early entrants in the streaming race have a decided margin lead, it is difficult to define which will be the dominant players in capturing and retaining eyeballs.

Some will succeed on a broad scale. Others will focus on niche segments, settling on smaller subscription numbers and will need to consider bundling with others for scale.

Profitable Growth â Consumers around the globe have become accustomed to having a steady stream of new video stories from their streaming services; and, as their entertainment costs rise, they add and delete options including PVOD and AVOD options. One size doesnâÂÂt fit all.

The old-timers of the streaming arena (Netflix and Amazon Prime) were hungry for growth beyond their home borders and had already begun moving cautiously before the world came to a screeching halt.

While they were required to produce content locally (typically 40 percent - as a prerequisite to signing subscribers in other countries,) they discovered people liked sitcom, superhero, sci-fi, action, fantasy, docs, adventure, drama, anima, mystery and even zombie films/series no matter where it was produced.

As a result, they quickly found Hollywood, Bollywood and Nollywood content was not good at home but often had a global market.

With more than 204M subscribers, Netflix was able to quickly acquire shows/films created in the EU, India, Africa, APAC and LatAm for their global entertainment hungry viewers.

As if that wasnt enough, Netflix signed a multi-year, exclusive window licensing deal with Sony for new projects as well as access to films/shows in their vault.

While a number of studios have pulled back their content from Netflix, HBO Max and Disney to shore up their related streaming services or to negotiate better alternative relationships; Netflix moved aggressively with U.S. as well as international studios to ensure a long-term steady flow of quality content for their audience.

Sony was one of the few studios that didnt rush to launch its own D2C service, choosing instead to focus on what it does best produce super content, anime and gaming.

To reinforce its own position, Sony acquired Central European Enterprises and Crunchroll from debt-burdened AT&T and put $200M into Epic Games and Unreal Engine, the driving forces in Hollywood production.

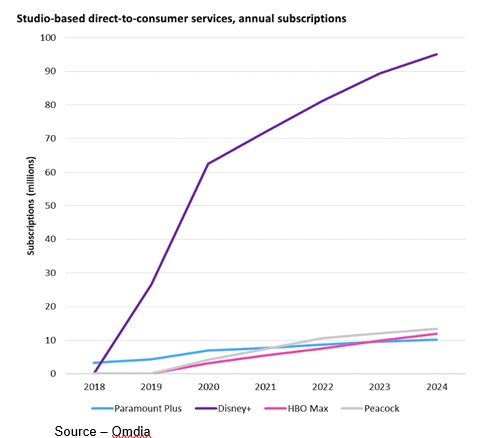

The phone folks used the funds to reduce its $147.2B debt, build out its 5G wireless infrastructure, reinforce WarnerMedia and support its fledgling HBO Max streaming service, which has about 43M subscribers at present with a target of 150M worldwide by 2025.

Aggressive but less visible than Netflix, Amazon added Prime Video service to its free delivery service to more than 200M subscribers worldwide and with its free (ad-supported) IMDb TV service, it is now used regularly by more than 83M registered users.Â

A few months before the pandemic, Disney rolled out Disney+; and despite a huge financial hit of having to temporarily shutter its parks, cruise lines and retail businesses, the company tripled down on content and expansion.

Â

Wind Rider Disneys CEO Bob Chapek wasnt shy about the companys rollout of Disney+ with a strong slate of films/series that had broad appeal and aggressively expanded beyond the U.S. to have a global presence. Of course, the companys strong entertainment image around the globe also added in its strong growth.Â

The company added Mouse House service in more than 50 countries (including India with its Hotstar division) to end the year with more than 100M subscribers and projecting it will reach 260M subscribers by 2024.Â

Finally, the companys parks cautiously reopened to families around the globe who are eager to get out of the house and have some fun.

While each streaming service is different with different products and different goals, it is easy for most of the media services to shape their discussion so they are not just surviving but leading.

For example, many question if Apple TV+ can remain viable in the aggressive content creation and delivery service with its modest library and business model.

But typical of Apple, it is playing by its own unique set of rules.Â

The company has more than 100M users (computers, tablets, phones) worldwide that use more than 1.5B active devices.

In addition, Apples entertainment library doesnt include just movies/shows, it also includes games, books and other media.

Lest we forget, Apples cash reserve is in excess of $192B that could easily be used to acquire any number of studios and their libraries as well as fledgling streaming services.

Thanks to a combination of issues, not the least being the family being locked home for days and weeks on end, many households took a close, hard look at their home entertainment budget and were dissatisfied.

The proliferation of ad-free and free with ad streaming services accelerated people cutting their cable and satellite bundle subscriptions.

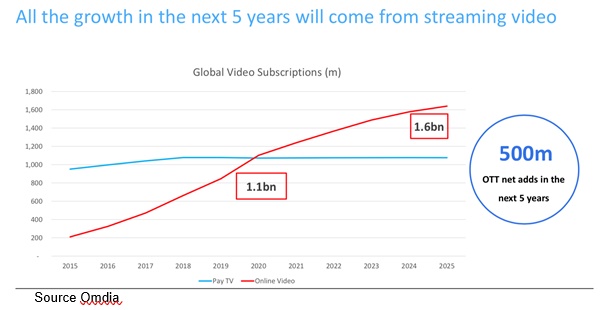

As we can see in the chart above video subscriptions jumped to 1.1B at the end of last year and is projected to grow to 1.6B in a few years.

But U.S. households 129M and global TV households 2B quickly found that like potato chips, you cant have just one.

Â

Lockdown and Bored With people being confined to their homes for much of last year, they broadened their streaming options slowly by adding new services to their existing entertainment options. It wasnât long before people settled on five options, adding and subtracting services as their interests changed.

So, they added a second and a third and

Yes, the combined cost of the new app options broadband service, SVOD, occasional PVOD and AVOD service is often equal to the restrictive bundle families left behind but the selection options and ability to watch what you want, when you want and on the screen you want has helped home budget managers justify the expense.

Â

Matter of Choice With plenty of viewable screens in the house, family members werent stuck with watching whatever the TV remote controller decided everyone should watch because now, they had service and screen choices of their own.

As youve found in your home, not everyone in the family wanted to watch the same film/show as everyone else in the household.

And as our technology usage has grown, so have the number of devices we can watch our content on.

Deloitte estimates that the average household has 11 connected devices and seven with screens TV, tablet, computer, phone.

The result has been a rush of general and specific streaming services bravely, boldly entering the marketplace.

There are the major Tier A services weâre all familiar with in the U.S. such as Netflix, Disney +, Amazon and, Hulu, which are commonly referred to as the big 4 in the U.S.,said Allan McLennan, CEP/Media, Head of M&E North America, Atos, Now, with a growing array of general audience competitors such as HBO Max, Paramount +, Peacock, Tubi, Pluto, Discovery+ and others, the category is not only gaining traction but establishing itself as the primary segment.

In addition, there are strong general appeal regional and country-centric services such as BritBox, TVMonde, MoviStar, Eduflix Italia, StarzPlay, Showmax, Vui, Stan, Kanopy, Gyao, Wowow, and more around the globe, McLennan added.

In the U.S., there are approximately 300 streaming services and globally more than 1,000.

There are no rules we can fall back on to determine which of the services will be winners or which will be losers, he emphasized, But we do know not everyone will still be here. In a few years, some will be acquired, and some will fail to find an audience.

Home or Away As movie theaters slowly/cautiously opened, people who simply had to enjoy the communal experience of seats in seats returned to the cinema while more people enjoyed the convenience of watching great films in the comfort of their living/family room. Options have proven to be a major boon to the content creation/distribution industry.

The rush of new streaming services has also opened up a lot of opportunities for indie filmmakers.

While filmmakers continually ask us for contacts at Netflix, Amazon and the other majors in hopes of selling their projects, most dont appreciate that all of the new streamers have expanded their sales opportunities and the new entertainment services have opened a world of opportunities for shooters/producers.

Film festivals around the globe such as Sundance, TIFF, SxSW, Tribeca, Berlin, Locarno, Tokyo, Palm Springs, Telluride, Busan, Sydney, Sarajevo, Cinequest and Paris are obvious opportunities for indies to get their works shown, seen and sold.

In addition, a growing number of filmmakers have had success at such events as the American Film Market and MIPTV.

If anything, the pandemic has helped the international film/show business as old and new streaming services search for the next big hit to attract more local and international subscription views.

Whether its a period drama, comedy, action thriller, horror, sci-fi, documentary or animated project; if it is a strong storyline, well shot and creatively posted, visual stories now have an unprecedented number of streaming sales opportunities McLennan emphasized.

Looking ahead, the sweeping restructuring of the M&E industry will become more aggressive, more defined.Â

The strategic pressure to acquire content that will meet the streaming servicesâ target markets will become increasingly important.Â

Streaming competitors require a steady investment in new content, marketing and technology that enables them to learn more about their audience and their viewing wants/needs.

Efficiency, effectiveness and success will be measured by subscriber acquisition and retention.

The way forward in the M&E industry especially for streaming services wont be for the faint of heart or for people who continue down the path the same way the industry grew in the past.

The future winners in the streaming arena will require gut decisions based on a comprehensive understanding of the data at hand and a steady stream of audience-satisfying content.

As Joe pointed out in The Sound of Metal, Serenity is no longer wishing you had a different past.